Process Benchmarking is benchmarking discrete processes against organisations with performance leadership in these processes.

Comparison of customer perception of goods and services supplied by the specific business unit against competing products and services in the same market.

Determining the attributes of both product and services, which the management feels influence the buying behaviour of customers.

Assigning weightages to all these attributes.

Rating of the company vis-à-vis its competitors against each of the above attributes.

Drawing a quality map where relative quality of all the companies is drawn against relative prices.

Conducting a survey to find out perception of the dealers/customers.

Identification of gaps in perception of the management and the customers.

Recommendations for improvements

A Systematic process for evaluating alternatives, implementing strategies and improving performances by understanding and adapting successful strategies from external partners.

Interfirm comparison (IFC) shows the management of a firm how its performance compares with that of similar enterprises, and draws management’s attention to areas of comparative weakness and strength within the business. This gives management an objective basis for judging the firm’s progress and effectiveness, and for improving performance by concentrating action on areas where improvement is most needed.

A true interfirm comparison is a carefully organised activity in the course of which firms in the same industry or trade agree to provide data on a voluntary and confidential basis to an organization that is trusted by all concerned to safeguard the confidential nature of the data supplied, and which is qualified and staffed:

Having obtained comparable data from participants, the orgnisation supplies each of them with a report including charts showing the data of all participating firms anonymously and in the form if ratios. Ideally, the set of ratios for each firm should be shown, together with some indication of the average and range of the results for each ratio. The report should explain how these data are to be used by the individual firm. The report shall- highlight points of weakness or strength as they are shown up by the IFC, interprets differences between the firm’s ratios and those of others taking part, and indicates the directions in which improvements might be made. The organisers of the IFC should also arrange t o have a senior member of their staff visit a participant, if desired, for discussion of its results.

The full results of the comparison are normally made available to participants only (otherwise firms would not go to the trouble of providing data, in depth and on comparable basis, as in needed for a proper IFC).

The whole emphasis of the exercise in on diagnosis and on giving individual firms an otherwise unavailable basis for improving their performance. It would, therefore, be wrong to think of IFC as being a kind of statistical survey. Those carrying out a statistical survey of an industry look at its firms in order to build u a general picture of some of its features; the picture is usually meant to be used for instance by government departments, trade associations, economists, or academics concerned with an industry as a whole. Such a survey aims at drawing general conclusions about an industry or part of it. An IFC, on the other hand, does not aim at drawing general conclusions, but at helping each participant to draw particular (and probably unique) conclusions about its own comparative position, its specific weaknesses and strengths, and the lines of action needed for improvement.

A distinction can be made between two kinds of IFC, one of these, which we shall call ‘type A’, aims at showing the management of each firm taking part how its overall success compares with that of the others and for what reasons of policy or performance its overall success differs from that of others. These comparisons relate to the business as a whole, and must, therefore, cover every significant aspect of performance. By the word ‘business’ is meant, in his context, a unit carrying out reasonably homogeneous and economically separate activities. It might be a separate company, or a division or subsidiary of a large group. Data relating to the performance of major departments of the business taking part will be covered in sufficient details to draw the attention of their general management’s to those specific matters that have caused the overall success of their business to compare favourably or unfavourably with that of others.

The second kind IFC, ‘type B’, sets out to concentrate on one or more specific aspects of performance in the participating firms-for instance, it may deal only with production efficiently or distribution efficiency. We shall refer to these as ‘partial’ comparisons.

Although annual comparisons are perhaps the most common, many IFCs are conducted on a shorter term basis, e.g. six monthly, quarterly or even monthly. Shorter-period comparisons are usually confined to simpler data, and can be supplemented by fuller comparisons at longer intervals (e.g. comprehensive annual comparisons). In some industries however, it may be appropriate to conduct full-scale comparisons quarterly, specifically to see how the trading pattern compares in different seasons. IFC is not to be regarded as a one-off exercise; projects are usually conducted on a regular basis, since only regularly repeated IFCs can provide participants with the monitoring service that enables them to check on a continuing basis their policy assumptions, targets, budgets, etc. Regular comparisons give up-to-date yardsticks of performance in changing trade conditions.

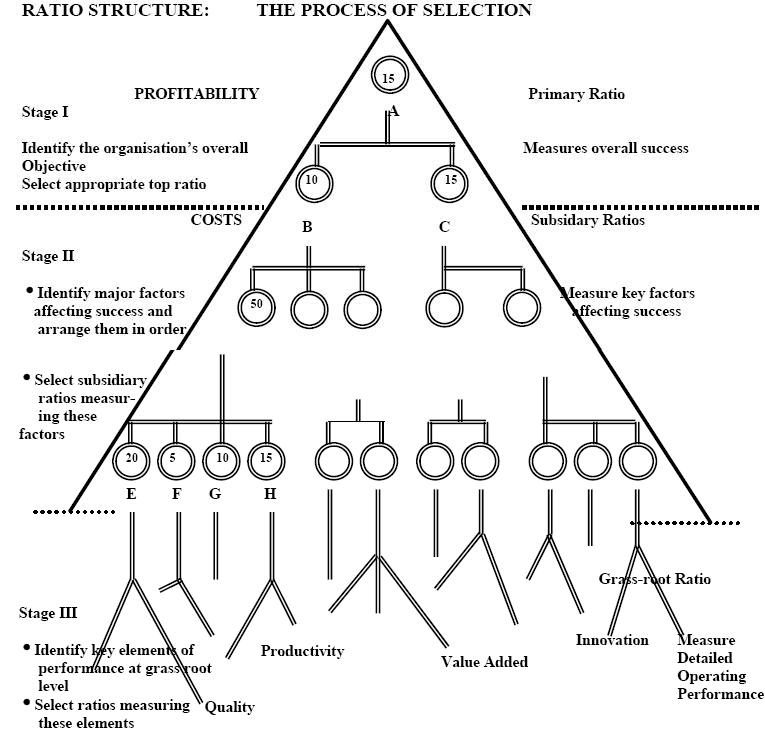

A very wide variety of management ratios is available, relating to many, different aspects of business operations including cost ratios, productivity ratios, profitability ratios, and ratios indicating financial structure and strength. The ratios can go into varying degrees of detail, and relate to various levels of the business, from overall operations down to details, of time taken per process or work-unit at shop floor level. It is not difficult to formulate as many as 1,000 ratios of one kind or another. However , this is obviously far too many for management use, and one is therefore faced with the problem of choice e.g., which out of the many ratios do we want and how are we to choose them?

Faced with this problem, proceed first to identify the level of management for whom the ratios are intended (for example, general management; management of a basic function; management of detailed operations within department of a factory). We then apply the Question, Answer, Measurement’ (QAM) principle to the choice of ratios. This process works as follows:

Stage -1

Question : What are the objectives of management?

Answer : In words (according to management level, function, etc.)

Measurement : A primary ratio or ratios measuring achievement of objective(s)

Question : What major factors affect attainment of objectives?

Stage-II

Answer:Identify and list the factors, in words

Measurement :One ratio for each major factor, if possible

Question :What further factors affect each of the major factors identified above?

Stage- III

Answer :Identify and list the detailed factors, in words.

Measurement :One ratio for each detailed factor, if possible. Further stages can be added, going into as much detail as is Required

The process is shown in general , abstract terms in enclosed figure.

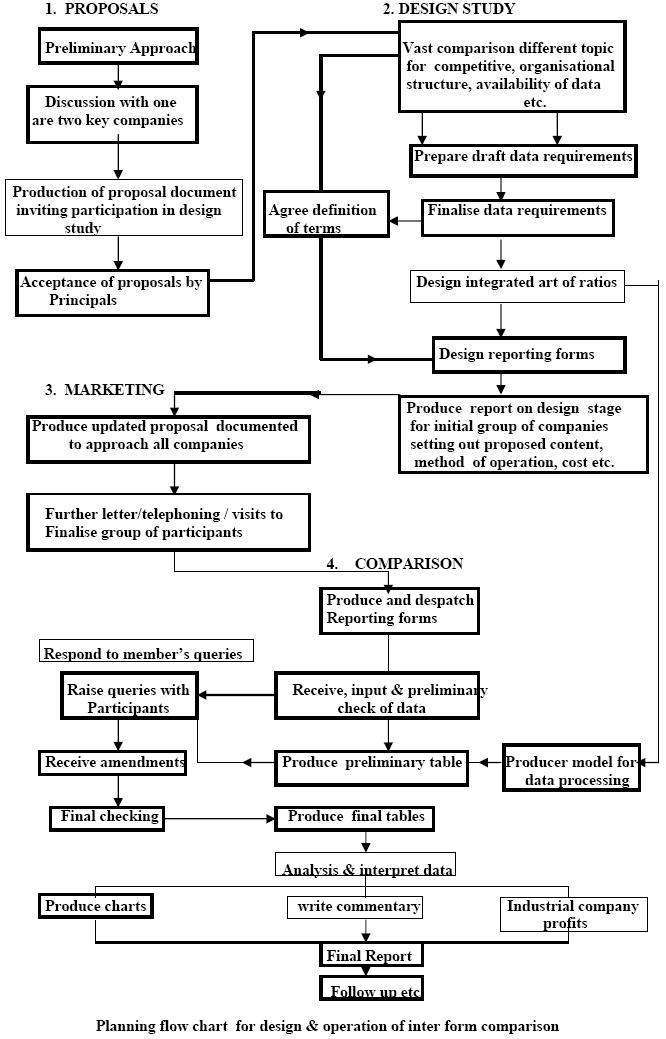

Marketing of the project will be based on this document which will be circulated to members of the industry or trade for whom the comparison has been designed. At the same time, this document can be supplemented by articles in the trade press, meetings, conferences, special seminars, etc. In fact, as a general rule, it is wise to discover early in the process of setting up a comparison in a new industry whether there is a trade journal – or if there are several, which is the leading one – and to approach the editor with the offer of a specially written article about the benefits of IFC in that industry,

The IFC scheme will be viable when a sufficient number of firms has registered for it, It is not possible to answer in general terms the question of what number of firms is need for a comparison. IFCs have been successfully conducted with as few as five firms, on the other hand, in some industries a much larger number may still be insufficient to give each of them the opportunity to compare its ratios with those of other sufficiently similar firms. The general aim is to give each participant a chance to compare with sufficient comparable firms and typically this might be anything between five and fifty-five firms.

Firms, which register for an IFC, are sent a reporting form prior to the site visit. After receiving the filled-in questionnaire code numbers are attached. Each year a firm, which renews its registration for a particular IFC, is given a new and different code number. Every care is taken to ensure that data checking and processing of questionnaires takes place under strict security conditions. Furthermore the results of the comparison show the data of firms anonymously under code numbers and in the form only of ratios and percentages. Another factor which reduced the chances of identifying firms figures in the tables is that the definitions of terms on which they are based are often different from those in published accounts; furthermore, the unit taking part in the IFC may not be the whole company whose figures appear in their annual accounts.

In finalising the scope and content of the comparison, one needs to balance the need for detailed data against the availability of the same.

The full results of the IFC are usually made available to participating companies only; participants have to go to some trouble and expense to provide this data on a proper basis; and if firms can obtain results without contributing data there is a real danger that the pool of comparative data will dry up. In some cases, however, extracts from the results are made available to non-participants. For example, there have been many instances in India where the IFC has been sponsored by some organisation with a particular interest in or responsibility for an industry sector. Such organisations have included Government ministries, Trade Associations and a number of Trade Promotion Bodies.

The questionnaires returned by participants must be carefully checked by the staff of the IFC team. The checking and investigating process is an essential feature of IFC and usually gives rise to a considerable number of queries, which must be raised and settled with the firms concerned. In some projects firms are asked to submit with their questionnaires audited copies of their most recent balance sheets and profit and loss accounts, because it has been found that a reconciliation of a firm’s figures with its audited accounts can assist in the checking process. The audited accounts cannot of course reconcile the fine detail of the IFC figures but they can be useful in establishing whether the full income is included; whether expenditure is of the right order; whether buildings have been included properly etc. It is very rare for firms to attempt deliberately to send wrong figures, because the usefulness of the IFC to them depends largely on the IFC team’s interpretation of their results. A firm, which deliberately sends in wrong figures, will receive an interpretation that is worthless to its management.

Once questionnaires have been checked and queries answered, the firms’ ratios are calculated. A ratio calculation programme is prepared for each project and the calculations may be performed by computer.

Tabulation of ratios is prepared when sufficient firms have contributed their data. It is the general experience of IFC organisations that some participants tend to be rather late in contributing their figures. This calls for a rigorous follow-up by phone, letter and personal visits.

In a good IFC scheme, each firm should be able to receive with its table of results three further documents. Firstly, a general report which describes the conduct of the comparison and draws the attention of participants to the points of relevance to all of them – showing, for instance, an analysis of profitability by size of company, type of business or any other major factor affecting results in broad terms. Secondly, each firm should receive guideline on how to use the ratios. This guide should explain to the reader the significance of key ratio. Thirdly a reporting visit should also be arranged if desired. As part of the process of helping managers to interpret and use ratios and interfirm comparisons, it is also useful to arrange seminars on these subjects. The seminars can either be of a general nature or organised to meet the needs and conditions of a specific industry or trade.

IFC study is followed by workshops and seminars for the interpretation of the ratios organised for all the participants. This could be followed by in-company workshops for identifying the functional and process improvement areas. These areas would be further analysed by the company for bringing in the improvements. The IFC team could also publish articles in professional magazines highlighting the results of the study.

Before a comparison can be embarked upon, there are a number of problems that must be overcome, both in the measuring of performance and the organisation of the project itself. Some of these problems are set out here and some solutions are discussed.

1.The Choice of Data – General Principles

A very great variety of performance ratios is available for possible inclusion in IFC ‘s for management and, in fact, over a thousand such ratios have been suggested at one time or another. It is advisable for the IFC participants and organizers to recognise the dangers of over proliferation of data and to approach the selection of data for comparison in a logical, systematic fashion. A good procedure is as follows:-

First, ask : For whom is the comparison designed? The answer may be : top management, or management of a particular function or activity in the firm.

Second :Choose performance data showing the target user how the performance for which he is responsible compares, and where and why it differs. The “approach to ratio selection is a useful way of ensuring the user gets the “how and why” performance data he needs.

Third : Consider what background data should be provided – not for general interest purposes but because it is usually related to specific performance data.

2.Measuring “overall” performance

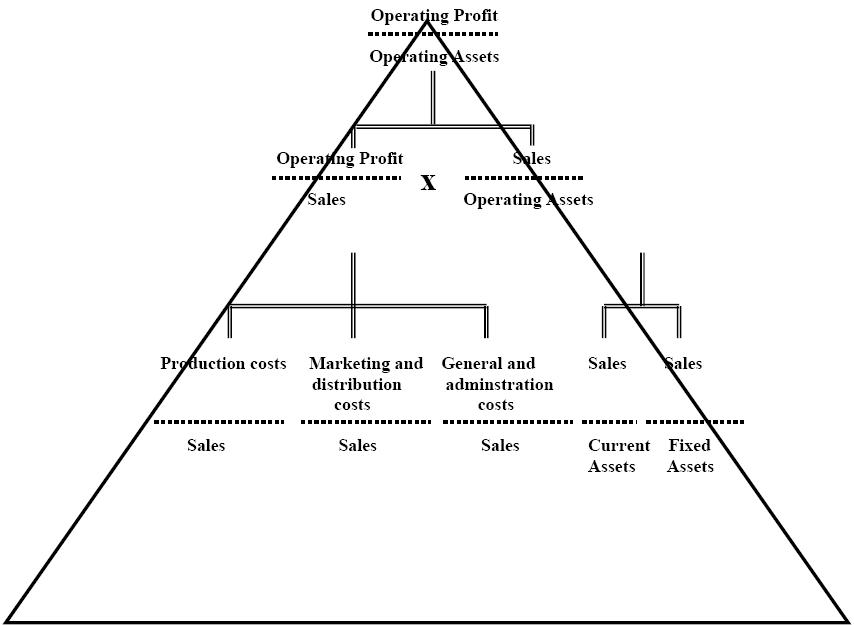

Many IFC’s are rightly aimed at helping the top management of the organisation. A problem here is that of arriving at an agreed overall indicator of performance. In comparisons relating to the operations of private enterprise firms, the objectives of the firms, and appropriate overall measures, are fairly clear, and usually agreed by most participants. The choice of a yardstick is therefore relatively straightforward in a manufacturing industry and many service industries the primary yardstick of operating performance is given by the ratio operating profit / operating assets.

In other sectors of activity (for instance in the public sector, and the operations of charities and other non-profit organisations) objectives are usually more complex and the measures suitable for private enterprise are not necessarily appropriate. Experience suggests that rather than aim at one overall ratio for agencies in such sectors, it is better to provide a number of indicators, which should always include indicators of economic viability plus indicators of the quality of service being provided.

3.Measurers of “Partial” Performance:

Some IFC’s relate not to overall business unit but to a specific aspect of operations (for instance the distribution function; the maintenance function}. It is sometimes more difficult to develop and justify simple single yard-sticks of performance at this level; often the ‘efficiency’ of a particular department can only really be judged in the context of operations as a whole. For instance, the eventual measure of a distribution department ‘s “efficiency” is its contribution to company profitability. However, if the comparison relates to companies making broadly similar types of product, single summary indicators can be used.

Examples are distribution costs expended per unit of output or weight of output, with further analysis to show the costs of various stage in the distribution chain.

4.Obtaining (and keeping) sufficient numbers of participants for a useful Comparison

This is obviously a basic feature of any successful IFC in the long-term, creating a real demand for IFC is basically an educational process; it is therefore important to ensure that IFC is featured in programmes of management education. Hopefully, such programmes will show the actual or potential manager how IFC works; what it involves for participants; and how the comparative results can be used. IFC should be presented as a standard management tool to be used on a regular basis, rather than as an activity in which an enterprise takes part once or twice in order to find the answer to all its problems.

5.Ensuring that participants use the results of IFC:

The basic principle here is that of good communications with participants. Examples of good communications include:-

6.Comparability of firms:

An objection to any form of comparison is that like is not being compared with like. This objection applies of course, to interfirm comparison. It is a point frequently raised by potential participants, who may say that firms in the industry are of different sizes, have different product ranges, production methods, etc.

The answer to this point is that the object of IFC is not to compare “firms” as such, but to see what effect certain differences in their features and practices have on relative performance. If there were no differences between the firms taking part they could learn nothing from the comparison. It is, however, important to take into account the differences, and this can be done by grouping results according to the factor in question (e.g. sizes, product range) or by providing a foot note.