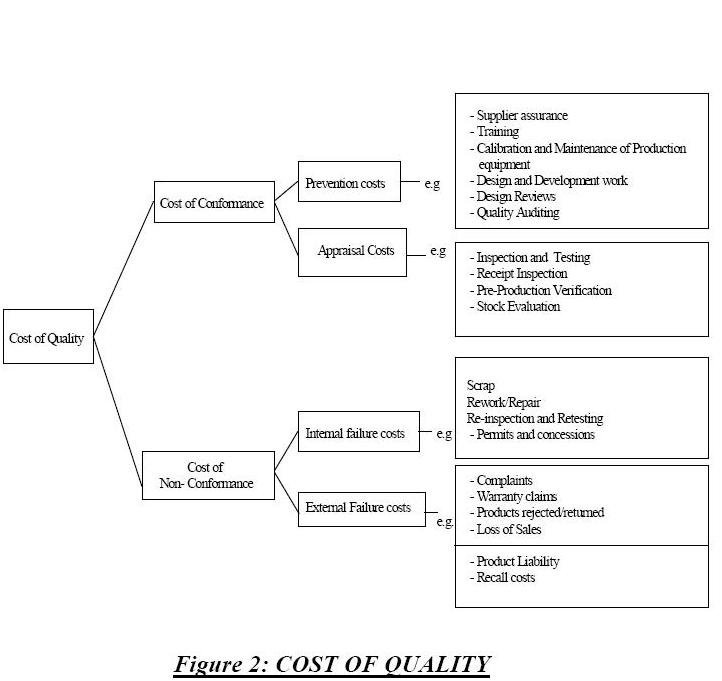

Cost of Quality or Quality Costs

There are significant cost benefits to be gained from implementing a QA system. The costs associated with implementing a Quality Management System can be broadly classified as Prevention costs , Appraisal Costs and Failure costs. Prevention costs are the cost incurred by an organization in implementing a Quality Management System. They include costs such as hiring an outside consultant, providing training to employees, creating the infrastructure for calibration, inspection and testing, etc. Before an organization implements a Quality Management System, these costs are negligible. However as the implementation gathers momentum these costs increase. The Appraisal costs are the costs of inspection and testing, pre production trails, inspection costs at suppliers premises, etc. These too are initially negligible and increase as a QMS is implemented. Failure costs can be broadly sub-divided into External Failure Costs and Internal Failure Costs. External Failure costs are costs associated with customer claims for failed or inferior products, loss of orders, legal costs,etc. Internal Failure Costs are costs incurred due to scrap, rejection, downgrading, blending, recovery, etc. These costs tend to be very high before a QMS is implemented. However as a QMS is implemented, there is a drastic reduction in the Failure costs resulting in an overall reduction in the total cost of Quality.

If we are to calculate the cost savings we first must determine the cost of quality.

It has been estimated that the average large American corporation using conventional methods of quality prevention, eg.- inspection and quality control, produces an after-tax profit of 4.8% of sales and has a cost of quality of approximate 20%. By changing the emphasis away from costs associated with non- conformance, then the cost of quality can be reduced and the savings go straight onto the bottom line of the profit account.

To obtain all the cost benefits an organization’s management need to maintain a highly visible approach to the reporting and monitoring of quality costs and where possible should relate them to other cost measures, eg.- sales, turnover, in order to :

(a) evaluate the adequacy and effectiveness of the quality management system

(b) identify additional areas requiring attention

(c) establish quality and cost objectives.

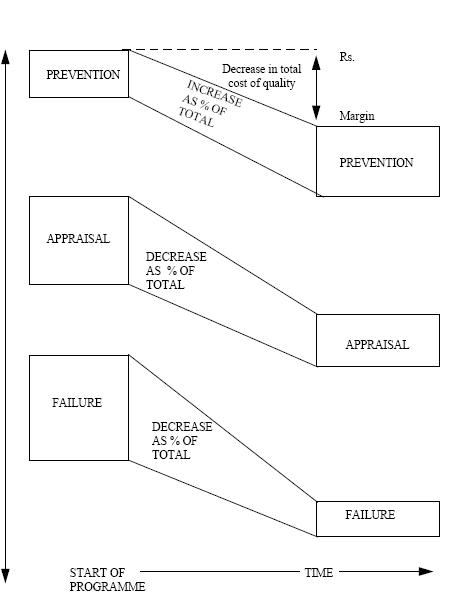

QUALITY PROGRAMME COST BENEFITS

Figure 1